We use cookies to give you the best possible experience on our website. By continuing to browse this site, you give consent for cookies to be used. For more details, please read our Online Terms & Conditions, Privacy Policy, Cookies Policy and Personal Information Collection Statement.

We recommend using a computer web browser or Hang Seng Mobile App to log on for enhanced security. Please visit "Security Information Centre" for more security tips.

Only 3 simple steps to apply online – Quote > Apply > Payment

![]()

Get up to $2,000 +FUN Dollars[1] with “3PROMO”

Successfully use promo code “3PROMO” to apply for this plan to enjoy extra rewards!

Offer 100% guaranteed monthly annuity income for 10 years to support your retirement expense.

You may apply for tax deduction[3] for the qualifying annuity premiums and save up to HKD10,200 per tax year.

You can choose from 4 premium options[4], with monthly or annual payment in HKD or USD.

Break even earliest at the end of 8th policy year

This plan reaches breakeven when the Guaranteed Cash Value exceeds the Total Premiums Paid[5].

Beneficiaries will receive the relevant benefit if the insured passes away during the policy term.

This plan has received 5-Star QDAP Award (Savings) in 10Life 5-Star Insurance Award 2026[6].

5 years

5 years

5 years

5 years

15 years

10 or 15 years

5, 10 or 15 years

5 years

3.30%

10 years:3.20%

15 years:3.30%

5 years:3.10%

10 years:3.20%

15 years:3.30%

3.10%

3.27%

10 years:3.15%

15 years:3.27%

5 years:3.02%

10 years:3.15%

15 years:3.27%

3.02%

10 years

10 years

10 years

10 years

The above information is intended as a general summary of information for reference only. Please refer to actual policy for the exact terms, conditions and exclusions of the Plan. If you wish to know more, please read the Product Brochure for details.

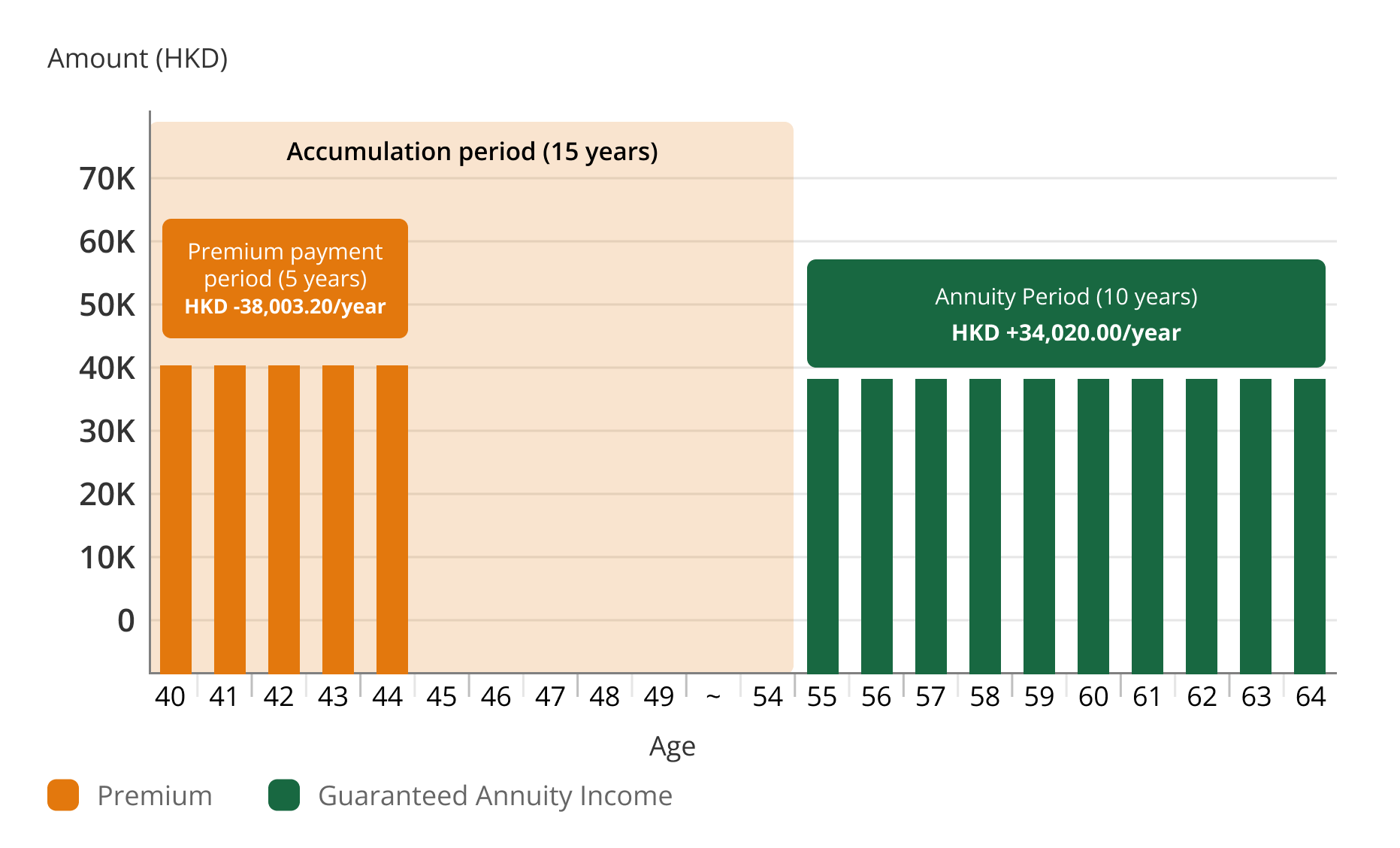

John (40) is an accounting firm manager who wants to start preparing for his retirement while enjoying tax deduction benefits[7].

Tax savings per year

HKD 6,460.54

Total premium

HKD 190,016.00

(HKD38,003.20 per year)

Total guaranteed annuity income

HKD 340,200.00

(HKD2,835.00 per month)

At the age of 40

John applies for the plan and starts a 5-year premium payment period

He pays HKD38,003.20 per year

During age 40 to 54

John's policy has a 15-year accumulation period, during which the total premiums paid will accrue interest until age 54

During age 55 to 64

John's policy enters the 10-year annuity period, he'll receive a guaranteed annuity income of HKD34,020 per year

Total income HKD340,200.00 (179% of the total premiums paid)

When the policy ends, the total guaranteed annuity income received is HKD340,200.00.

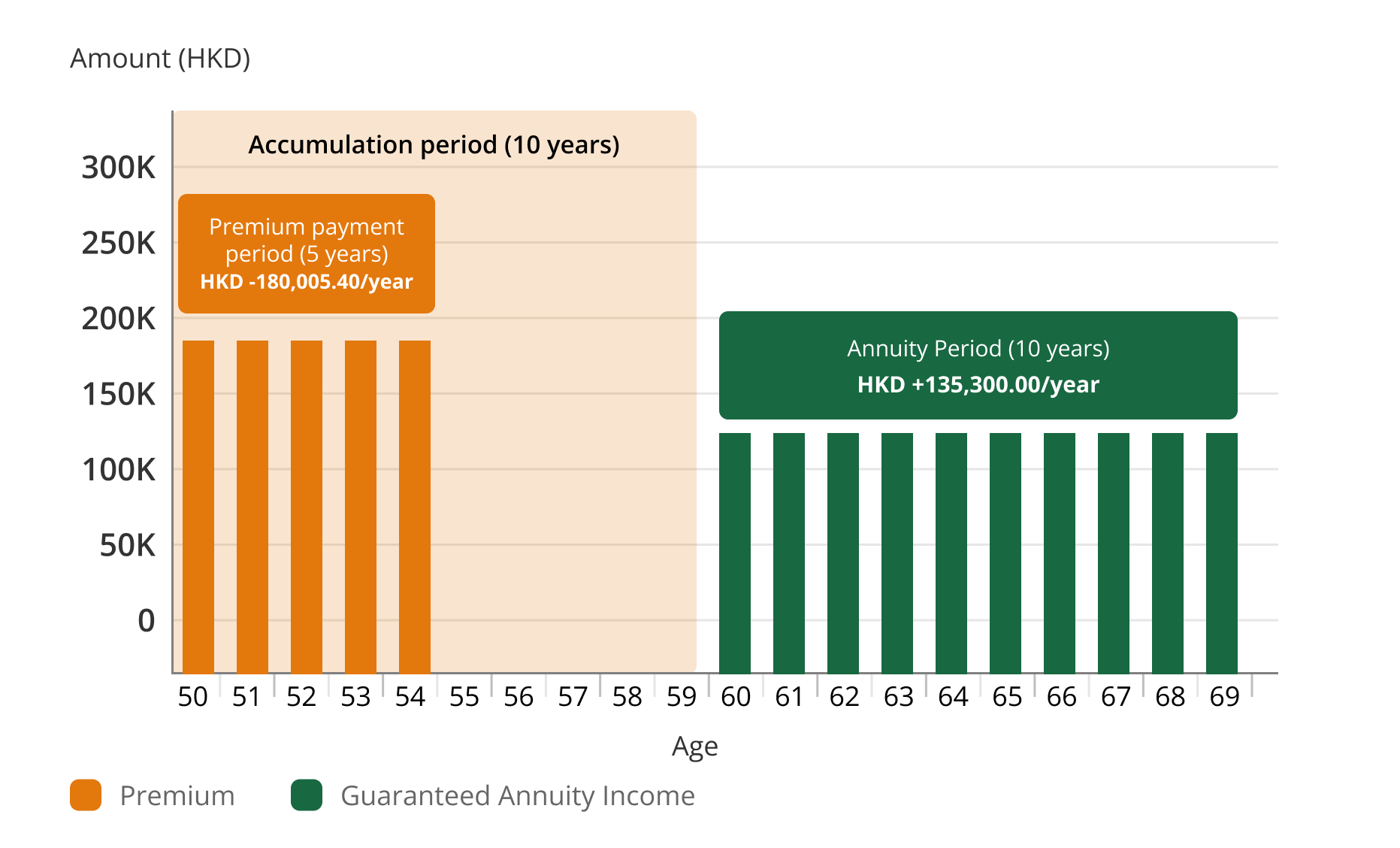

Peter (50) and Alice (45), married for 20 years, want to save up for retirement while enjoying tax deduction benefits[8] from QDAP.

Tax savings per year

HKD 20,400.00

Total premium

HKD 900,027.00

(HKD180,005.40 per year)

Total guaranteed annuity income

HKD 1,353,000.00

(HKD11,275.00 per month)

At the age of 50

Peter applies for the plan and starts a 5-year premium payment period

He pays HKD180,005.40 per year

Since both are taxpayers with taxable income and Alice doesn't apply for any tax-deductible products[8], Peter can allocate the premium to Alice for tax deduction. This way, they can jointly claim a maximum tax deduction of HKD120,000 (HKD60,000 per individual) per year.

During age 50 to 59

Peter's policy has a 10-year accumulation period, during which the total premiums paid will accrue interest until age 59

During age 60 to 69

Peter's policy enters the 10-year annuity period, he'll receive a guaranteed annuity income of HKD135,300.00 per year

Total income HKD1,353,000.00 (150% of the total premiums paid)

When the policy ends, the total guaranteed annuity income received is HKD1,353,000.00.

This plan has been certified by the Insurance Authority (IA) as Qualifying Deferred Annuity Policy (QDAP) in Hong Kong. It's a life insurance plan with savings elements and isn't equivalent or similar to any kinds of bank deposit. It's underwritten by Hang Seng Insurance Company Limited.

An annuity is a long-term insurance product. The purpose of an annuity is to help policyholders convert their money into a steady stream of income over the long term. It helps policyholders spend their retirement savings in a disciplined way to address the financial risks brought about by longevity. The policyholder pays the premium to an insurance company which will provide regular annuity income to the policyholder immediately or after a designated period of time or after a certain age of the policyholder, for the period specified in the contract.

QDAP is a deferred annuity product that complies with the guidelines issued by the Insurance Authority (“IA”) and certified by the IA. Taxpayers are eligible to claim a tax deduction for their qualifying deferred annuity premiums, and the policies must meet certain requirements, for example:

For details, please visit IA’s website.

To facilitate your completion of tax returns, HSIC will issue an Annual Summary of QDAP. Please note that for new applications, only QDAP policies issued and with premiums received by HSIC on or before 31 March will have their policy details included in the Annual Summary of Qualifying Deferred Annuity Policy for that relevant tax assessment year.

The Annuity Income during Annuity Period will be paid according to how you paid your initial premium payment. Here're the arrangements:

If you want to change how you receive your Annuity Income, please contact Hang Seng Insurance at (852) 2596 6262.

The income payout of many deferred annuity products in the market is usually divided into two parts, namely “guaranteed” and “non-guaranteed”. “Non-guaranteed” return is often affected by other factors such as the investment return, claims and profits of the insurance company. In an extreme case, the “non-guaranteed” return could be zero.

On the other hand, the annuity income payout of eIncomePro Deferred Annuity Plan (100% Guaranteed) is 100% guaranteed, without any “non-guaranteed” part.

Lifetime annuity means that annuity income will be distributed to the policyholder till the designated age (aged 100 to 120) or even death. Term annuity means there is a designated annuity period, usually 10 to 20 years. In theory, for the same amount of total premium paid, the longer the annuity period, the less the amount of annuity income, and vice versa. Therefore, applicant should choose the appropriate plan type based on your financial needs.

Accumulation period refers to the period before the start of the annuity period. It includes the premium payment period, which allows the policy value to grow through investment by the insurer.

The Internal Rate of Return is a way to calculate the return. “Internal” means only the relevant cash flows are calculated, including the invested capital (e.g. premiums), withdrawn amounts (e.g. annuity income) and the time factor. External factors (e.g. inflation rate) are not considered.

A QDAP must satisfy the criteria set out in the guideline issued by the Insurance Authority (IA). One of criteria is that annuitant must be at the age of 50 or above when receiving the annuity income. Hence, options of accumulation period available might vary subject to the life insured’s age.

| Premium Payment Term (Year) |

5 | ||

| Accumulation Period (Year) |

5 | 10 | 15 |

| Annuity Period (Year) |

10 | ||

| Insurance Age at Issue | 45 – 64 |

40 – 64 | 35 – 60 |

Yes, you may apply online for more than one eIncomePro Deferred Annuity Plan (100% Guaranteed) policy.

If you would like to apply for more than one policy of eIncomePro Deferred Annuity Plan (100% Guaranteed), please note that your total premiums paidIncluding the total premiums paid for following plans (including application in progress and in-forced policies): (1) Income Step-up Life Insurance Plan, (2) Income-Select Life Insurance Plan, (3) Smart Income Life Insurance Plan, (4) Step-Up Income Life Insurance Plan, (5) Target Income Life Insurance Plan, (6) RewardYou Life Insurance Plan, (7) SavourLife Annuity Life Insurance Plan, (8) SavourLife II Annuity Life Insurance Plan, (9) SavourLife II (RMB) Annuity Life Insurance Plan, (10) HarvestLife (RMB) Life Insurance Plan, (11) The Choice 5-YearLife Insurance Plan, (12) FutureEnrich Life Insurance Plan, (13) MaxiAnnuity Life Insurance Plan, (14) PrimeLife Deferred Annuity Life Insurance Plan, (15) MaxiPlus Annuity Life Insurance Plan, (16) FortuneLife Deferred Annuity Life Insurance Plan and (17) eIncomePro Deferred Annuity Plan (100% Guaranteed)for all life insurance plans in HSIC cannot exceed HKD40,000,000.

eIncomePro Deferred Annuity Plan (100% Guaranteed) only has one annuity income option. Monthly guaranteed annuity income will be distributed on each monthiversary starting from the commencement date of the Annuity Period.

Customer can choose to pay the premium in HKD or USD for the USD policy of this Plan. We only accept USD payment from USD bank account of Hang Seng Bank. If customer chooses to pay the premium of USD policy in HKD, the relevant amount will be converted to USD subject to market-based prevailing exchange rate as determined by HSIC when processing the premium payment, whereas this exchange rate is subject to market fluctuation and will have a direct impact on the amount of the premium payment in HKD.

eIncomePro Deferred Annuity Plan (100% Guaranteed) offers a grace period of 30 days for payment of any premium when due. If a premium is not paid by the end of the grace period and the Non-forfeiture Value is sufficient to cover the amount of the relevant unpaid premium, the terms of Automatic Premium Loan will immediately take effect to pay the relevant unpaid premium. If the Non-forfeiture Value is insufficient to cover the amount of the relevant unpaid premium, the policy will immediately lapse.

eIncomePro Deferred Annuity Plan (100% Guaranteed) can only be applied via online platform.

Once you complete the online eIncomePro Deferred Annuity Plan (100% Guaranteed) application form, you will be asked to confirm and verify your details on a preview page. The same day, a confirmation email will be sent to the email address you provided in your application, assuring you that your application of this deferred annuity plan has been received. We will notify you regarding the application notification by sending a SMS to your default mobile number on record at Hang Seng Bank within 7-10 working days under normal circumstances, and the policy will be delivered to your default postal address on record at Hang Seng Bank once your application is approved. This simplified process frees you from the hassle of typical insurance applications. You can also call our hotline at (852 )2198 7838 for queries.

If you are a Hang Seng Bank Personal e-Banking customer, you can manage your policy(ies), check policy information 24/7 via Personal e-Banking (Insurance Overview Desktop version). You may also call our hotline at (852) 2596 6262 for queries about your policy.

Hang Seng Insurance Company will issue an Annual Summary to you within 40 days after the end of the year of assessment (i.e. 31 March), listing the total amount of qualifying deferred annuity premiums you paid during the year of assessment.

You can find all the forms and documents here for our insurance products.

Service hours (excluding public holidays):

Mon to Fri: 9:00 a.m. to 5:45 p.m.

Sat: 9:00 a.m. to 1:15 p.m.

I can answer insurance details and application procedures

I can answer insurance details and application procedures

Chat with H A R O now